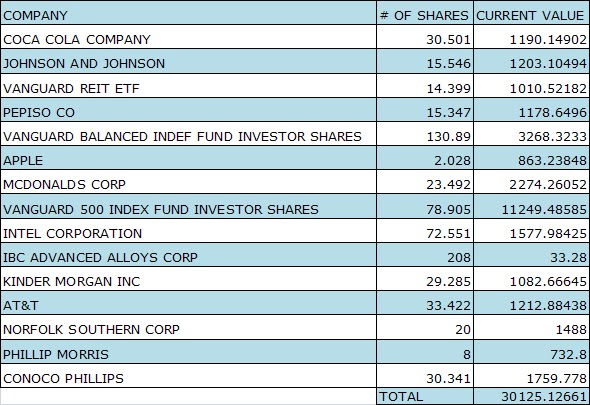

What really matters in my journey to FI are these posts right here. My expense posts outline my spending every month. It shows my offensive and defensive strategies and just how well they are working. Offensive is my income. Am I making the best use of my time or am I just slagging off on the weekends. Defensive is my spending. How well am I controlling my urges to buy the latest widget or gadget? How often to I really need go out to eat with my buddies? Let's take a look:

Income:

Paycheck: ¥299,404

Part Time Job: ¥102,755

Part Time Job 2: ¥27,000

Questionnaire: ¥5000

Total: ¥434,159

My income was pretty insane this month. I received my regular pay in addition I discovered some unused vacation time at my part time job and asked to receive the whole lump sum ASAP (got to get that interest working in my favor). The Step EIKEN test was also held where I am an interviewer (part time job 2). In addition a friend introduced me to a survey where for answering almost 400 questions in Japanese and 400 questions in English I can earn ¥5,000. Not bad, but I have to admit it was a drag getting through it all in one sitting. Over all this might have been my best month ever as far as income goes.

Expenses:

Expenses weren't out of line with where they usually are. I suppose because of "Presents" it was a bit high. This year I sent out my X-mas album late and so, I paid off my credit card in the month of February. I track my bills by when I actually pay them so this expense landed in the second month of the year. This should be the last month that "BIlls" will be as high as it is. I'm completely clear of my old cellphone bill now, and riding high on prepaid.

My target savings rate for the year is 55%. So far I've hit:

January - February: 47.36%

February - March: 65.43%

My average savings rate for the year is 56.40%. Not bad! It looks like we are back on track. I'll admit that March - April is already shaping up to be a bit of a struggle with end of year school parties, a bike trip, and possibly a fun weekend at Fujikyu Highlands. I'm all about enjoying my money while I have it as well, but I am sure not gong to forget about my goals.